Key Takeaways

- Two major expansions of the Child Tax Credit — one in 2017 focused on simplification and one in 2021 focused on generosity — represent two distinct approaches to supporting families in the tax code.

- Both expansions are steps in the right direction. Simplifying tax credits and making them more generous are complementary goals that policymakers should consider pursuing in tandem as part of a more comprehensive package.

- There are several overlapping tax benefits for families with children in the federal tax code, including the Child Tax Credit (CTC), Earned Income Tax Credit (EITC), child and dependent care tax credit (CDCTC), and head of household (HoH) filing status.

- We analyze options for further rationalizing this maze of family tax benefits by shrinking or eliminating them in conjunction with an expansion of the CTC.

- Our findings suggest there is still much to be gained by considering further rounds of family tax benefit consolidation. Each of the options we consider here keep the poverty impact of a more generous CTC while reducing overall costs, complexity, and work/marriage penalties.

Introduction

The Child Tax Credit (CTC) saw two major expansions in the last decade. In 2017, Congress combined two existing child-related tax benefits – the dependent exemption and the Child Tax Credit – into one expanded and more generous CTC worth up to $2,000 per child. In 2021, Congress temporarily expanded the CTC by eliminating the phase-in and increasing the credit amount to $3,000 for older children and $3,600 for younger children.

Both expansions were steps in the right direction, but they represent what have been two distinct approaches in American public policy. The first is focused on rationalizing or streamlining our complex system of child-related tax benefits. The second is focused on increasing the generosity of child-related tax benefits. American families would benefit from reforms that do both, but proposals to rationalize and expand the CTC have been few and far between in recent years.1 A major expansion of the CTC akin to that temporarily implemented in the 2021 American Rescue Plan Act would be very expensive and leave excessive tax code complexity as well as work and marriage penalties untouched. Consolidation defrays the cost of expansion and helps the interlocking parts of the tax code function more smoothly. However, critics of tax benefit rationalization have often viewed it with suspicion, assuming any such efforts are a Trojan horse for backdoor cuts. This view is mistaken—there is much to be gained from pairing expansion with consolidation without sacrificing poverty reduction.

Our existing maze of family tax benefits — including the CTC, Earned Income Tax Credit (EITC), child and dependent care tax credit (CDCTC), and head of household (HoH) filing status — has several structural deficiencies that make overhauling the system a prerequisite for any effort to boost support for families with children. The report offers several options for expanding and streamlining family tax benefits to address these issues.

We begin with four principles that policymakers should consider when designing family tax benefit reforms. A pro-family policy package should:

Support children in need. Poverty has a detrimental impact on children’s development and later life outcomes. The 2021 expansion of the CTC was responsible for a major reduction in child poverty. The provisions increasing the generosity of the credit and eliminating the earnings requirement were the most important drivers of this reduction.2 The main lesson is that future proposals should continue to focus on boosting benefits for the lowest-income families.

Support marriage. Children do best when raised in two-parent families. Family formation is a complex process, but one of the factors that hinders marriage are penalties in our tax and transfer system, particularly for couples with children.3 Reducing or eliminating these marriage penalties should be part and parcel of future proposals to expand family tax benefits.

Support parental choice. Parents have a range of options when it comes to balancing work and family life. In some households, both parents work full-time, while others prefer one parent to work full-time while the other cares for children at home. Some households prefer center-based care while others prefer home-based or relative care. Reforming tax benefits to avoid privileging some arrangements over others and achieve child care pluralism is an important goal for family policy.4

Support upward mobility. The proliferation of income-tested programs, which phase out as household earnings rise, has helped reduce child poverty but also increased implicit marginal tax rates (IMTR) on poor and working-class families. Reforms to the tax and transfer system in the 1990s reduced IMTRs on those moving from welfare to work but increased them on working families striving to join the middle class.5 Reducing these high implicit marginal tax rates should be a priority in the overhaul of family tax benefits.

These principles are not new — they have guided previous efforts to rationalize family tax benefits over the last three decades. Writing in 1991, economists Eugene Steuerle and Jason Juffras looked at the American tax and welfare system and found a mess. There were several distinct programs aimed at supporting families with children, but they were structured as a kludgy system of overlapping benefits, which were often at odds with each other. Families trying to navigate this system learned three lessons from it — don’t move, don’t work, and don’t get married — because the system would impose hefty penalties on you if you tried.

To address these issues, Steuerle and Juffras proposed replacing the dependent exemption and a portion of Aid to Families with Dependent Children (AFDC) with a universal fully refundable Child Tax Credit. The result would be a set of reforms that reduced child poverty alongside work and marriage penalties. The National Commission on Children integrated this proposal into its landmark report on building an agenda for American families.6

But Congress had other plans. Instead of simplifying family benefits, legislators added more complexity by increasing the generosity of the EITC and varying it based on family size for working-class families in 1993 and adding a nonrefundable CTC on top of the existing dependent exemption for middle-class families in 1997. By 2013, the family tax “kludgeocracy” had grown by leaps and bounds.7

In 2017, Congress finally took the first step to reverse the tide. The Tax Cuts and Jobs Act (TCJA) eliminated personal exemptions and replaced them with a larger standard deduction and CTC – reducing the total number of major child-related tax benefits from five to four. In 2021, Congress passed important expansions of the CTC and EITC as part of the American Rescue Plan Act, but in doing so reverted back to their bad habit of expansion via kludge.

Congress can do more by building on the 2017 and 2021 reforms but taking lessons from previous federal efforts.8 This report offers three options for improving ARPA-style proposals by integrating insights from TCJA and previous consolidation efforts that boost marriage, work, and parental choice.

The baseline expanded CTC

In 2021, Congress temporarily expanded the CTC in several important ways, including 1) raising the maximum credit amount from $2,000 for children under 17 years old to $3,000 for children aged 6-17 years and $3,600 for children under 6 years old, 2) eliminating the earnings requirements (colloquially called full refundability) so families with no earnings received the full credit, 3) adding an intermediate phaseout threshold of $112,500 for single parents and $150,000 for married parents, and 4) paying out the credit in monthly installments.9

This expansion, which has been proposed in several similar versions since 2021, provides our baseline for analysis of further reforms.10 We use PolicyEngine, an open-source software platform that computes the impact of public policies, to estimate the cost and distributional impact of our baseline proposal and additional reforms.11

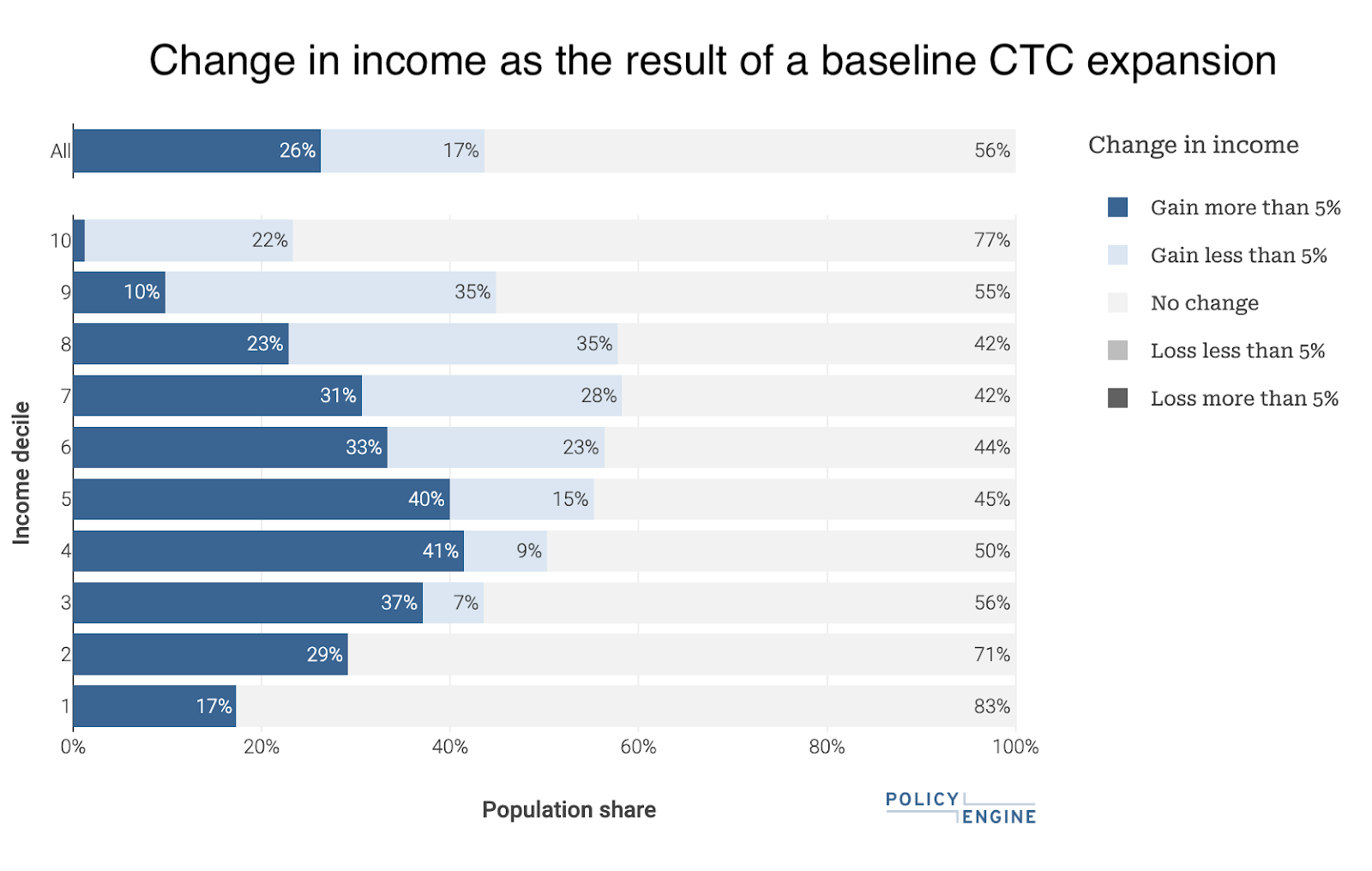

This baseline expansion of the CTC would cost an additional $109.7 billion in 2024 and reduce child poverty by 31.2 percent.12 Figure 1 shows the distributional impact of the changes. 44 percent of the population would see a net gain in income, with the largest increases going to middle-class households. No households are made worse off in this scenario.

Figure 1

Despite these positive impacts, this expanded CTC could be substantially improved by consolidating it with other credits — including the head of household filing status, the Child and Dependent Tax Credit, and the Earned Income Tax Credit — in order to reduce overall costs, shrink or eliminate problematic features related to marriage penalties, loosen limits on parental choice, lower barriers to upward mobility, and generally reduce complexity related to overlapping benefits for households with children.

The following sections consider each of these reforms in turn, describing how they work, problems with the structure of current benefits, and the impact of eliminating or shrinking them in conjunction with this baseline expansion of the CTC.

Supporting marriage by replacing the head of household filing status

Research makes clear that children do best when raised in a stable two-parent household and that marriage is the best institution for supporting families with children. Despite growing evidence around the importance of marriage, the share of births to single mothers has nearly doubled over the last 40 years.13 As for any other major life choice, many factors influence an individual’s decision to marry, cohabitate, or remain single. This includes economic factors such as education, employment, and even taxes.14

The tax code can penalize marriage when two individuals face a higher effective tax rate because they get married and file jointly rather than remain single. Studies find that these marriage penalties, if large enough, reduce the probability of couples getting married.15 Congress has spent considerable time and effort reforming the tax code to reduce marriage penalties over the last 25 years, including major changes in the Bush tax cuts of 2001 and the Trump tax cuts of 2017 that reduced them for many middle- and upper-income households.

Despite these reforms, lower- and middle-income households with children still face some of the heftiest marriage penalties in the tax code.16 A major source of marriage penalties for single parents that has received relatively little attention from policymakers is the head of household filing status.17

When they file taxes, households have the option of itemizing deductions or taking the standard deduction. The 2017 tax reforms, which eliminated personal exemptions and replaced them with a larger standard deduction, increased the overall proportion of households who choose to take the standard deduction. A household’s filing status also determines their tax bracket thresholds.18 There are three main options for filing status that determine the size of the standard deduction and bracket thresholds — single, married, and head of household (HoH). The tax code minimizes marriage penalties by ensuring the standard deduction and tax bracket thresholds for married couples are double those of single couples for low and middle-income households.

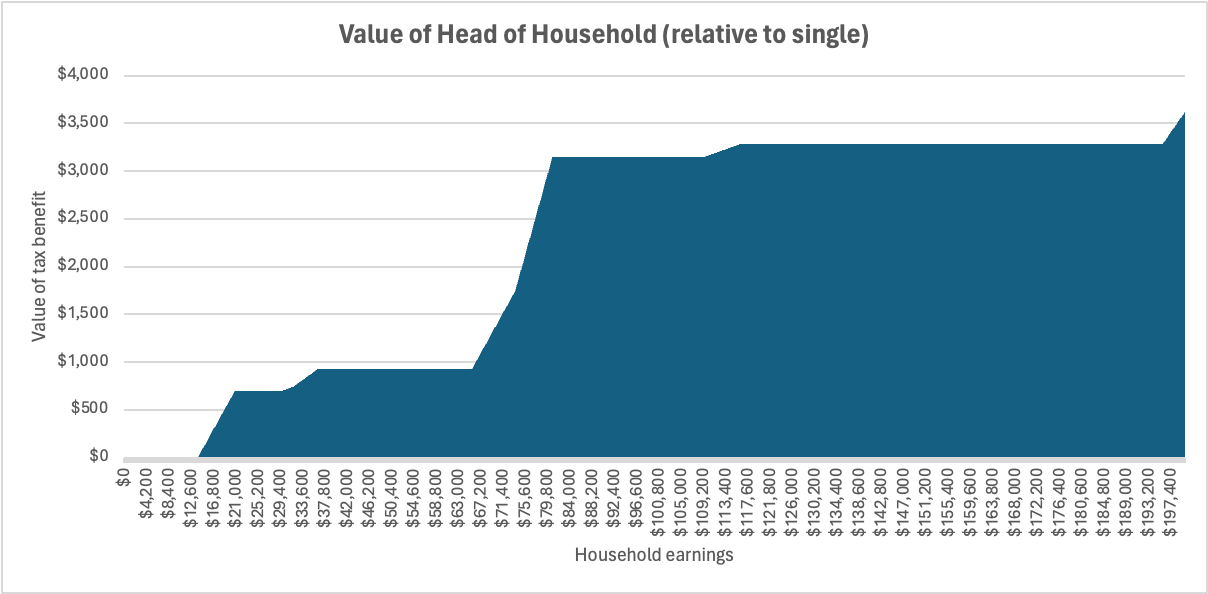

Single individuals caring for dependents – often children – can file as head of household. HoH filing status has two components: wider bracket thresholds relative to single filers (for the 10 percent, 12 percent, 22 percent, and 24 percent brackets) and a more generous standard deduction amount relative to single filers ($20,800 versus $13,850 – a $6,950 difference – in 2023). A similar filing status is not available to married couples caring for dependents. Figure 1 breaks down the value of filing as head of household relative to single between these two components – a more generous standard deduction and wider bracket threshold. Several features of the HoH filing status stand out.

Figure 2

As the only remaining child-related tax exemption, it is much more valuable to high-income earners relative to low-income earners. Whereas it amounts to $615 for a single parent making $20,000, it is worth $3,616 for a single parent making $200,000. In contrast to other family-related tax benefits, the value of HoH filing status does not vary with the number of children in the household. A single mother with one child receives the same benefit as one with three children.19 Crucially, the HoH filing status also imposes substantial marriage penalties on households with children. Low- and middle-income parents, for example, may find themselves paying up to $1,000 in additional taxes each year if they get married.20

The most straightforward way to address each of these issues is to sever filing status from the presence of children by eliminating the head of household filing status – single parents would simply file as single – and replace it with an expansion of the CTC. This would eliminate the last “upside down” provision (where the value of the benefit increases with income) in the federal tax code for dependents left in place after the 2017 reforms. Various experts have recommended iterations of this proposal, including the 2005 President’s Advisory Panel on Federal Tax Reform and the 2008 report of the Taxpayer Advocate.21

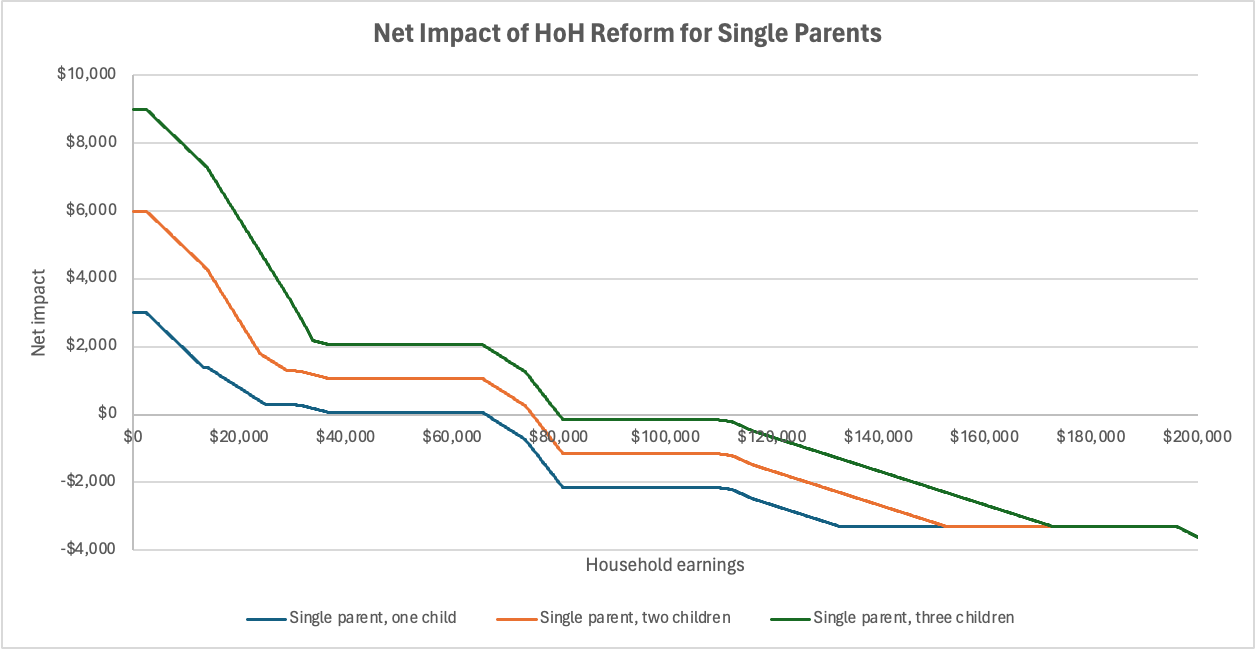

The distributional impact would depend on the value and structure of the expanded CTC. Figure 2 illustrates the net impact on single parents by income. It assumes children are older than six years old with each receiving a $3,000 credit. Under this ARPA-style expansion, most single parents, particularly poor and working-class households with multiple children, would be better off. Some middle- and upper-income single parents, who previously received the largest benefit, would see reduced tax benefits in some cases but also reduced marriage penalties.22 Married parents would all be better off.

Figure 3

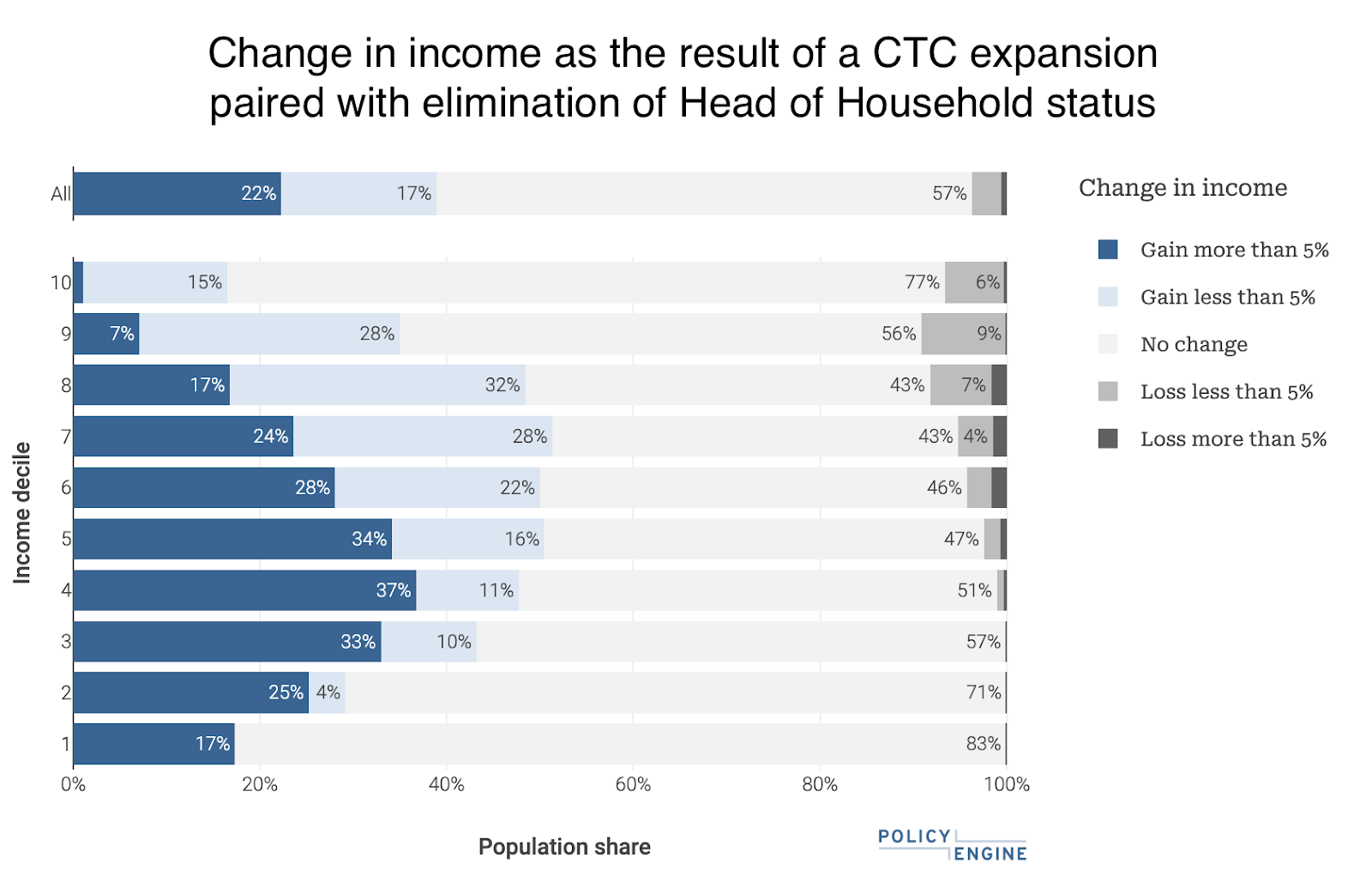

In our analysis, eliminating the head of household filing status alongside an expansion of the CTC would cost a total of $83.8 billion in 2024 — saving about $26 billion relative to our baseline CTC expansion — and reduce child poverty by 30.9 percent – nearly the same as our baseline.23 Figure 4 shows the distributional impact of the changes. 39 percent of the population would see a net gain in income, with the largest increases going to middle-class households. Four percent of households are made worse off in this scenario. They are in the middle and upper deciles.

Figure 4

Supporting parental choice by replacing the CDCTC

Parents of young children can, in theory, rely on an additional source of tax relief to help them manage the costs of caring for their children. The Child and Dependent Care Tax Credit (CDCTC), first established in 1976, grants parents a credit against a share of their child care costs. In practice, the credit is onerous to claim and too complex for parents to plan around. It also discriminates against larger families and limits parental choice about what care best suits their family’s needs.

The CDCTC is intended to support working parents by allowing them to defray some of the cost of care that enables them to work. The credit is limited to households where all parents have earnings — a family with a stay-at-home parent is not eligible for the credit, even if child care is part of what enables the other parent to work. To claim the credit, parents track and report total spending on child care, subject to a cap, and then are reimbursed for a portion of their spending. The percent that is reimbursable varies by income, while the caps are static. The credit caps the reportable expenses a family can claim at $3,000 for one child or $6,000 for two or more children. The percentage of that spending that can be claimed as a tax credit increased with income (in theory) to a maximum of 35 percent for families with an Adjusted Gross Income of $15,000 or less. For families making more than $15,000, the eligible percentage of expenses is reduced linearly until it reaches 20 percent of eligible expenses for all families earning $43,000 or more.

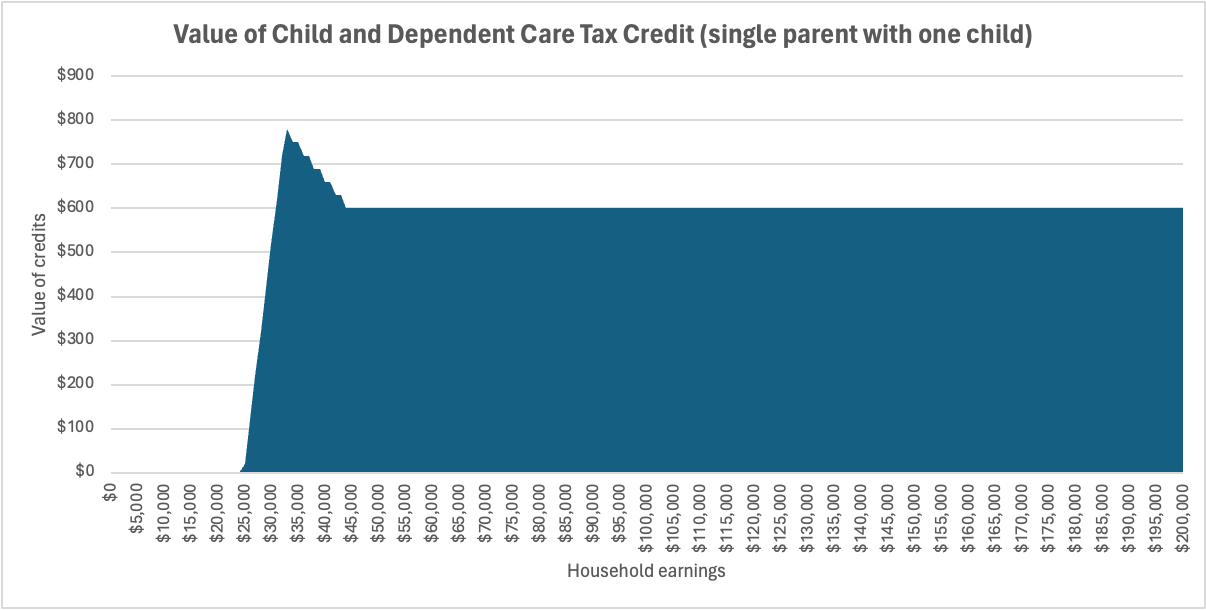

On paper, that means the maximum value of the credit is $1,050 for one child or $2,100 for two or more. But in practice, because the credit is not refundable, families making less than $25,000 are not eligible to claim it at all, because their tax liability is too small (see figure 5). Thus, the 35 percent credit rate is largely vestigial. Most families with enough income to qualify are claiming the CDCTC at the minimum refundability level of 20 percent, making them eligible for up to $600 for one child or $1,200 for two or more.

Figure 5

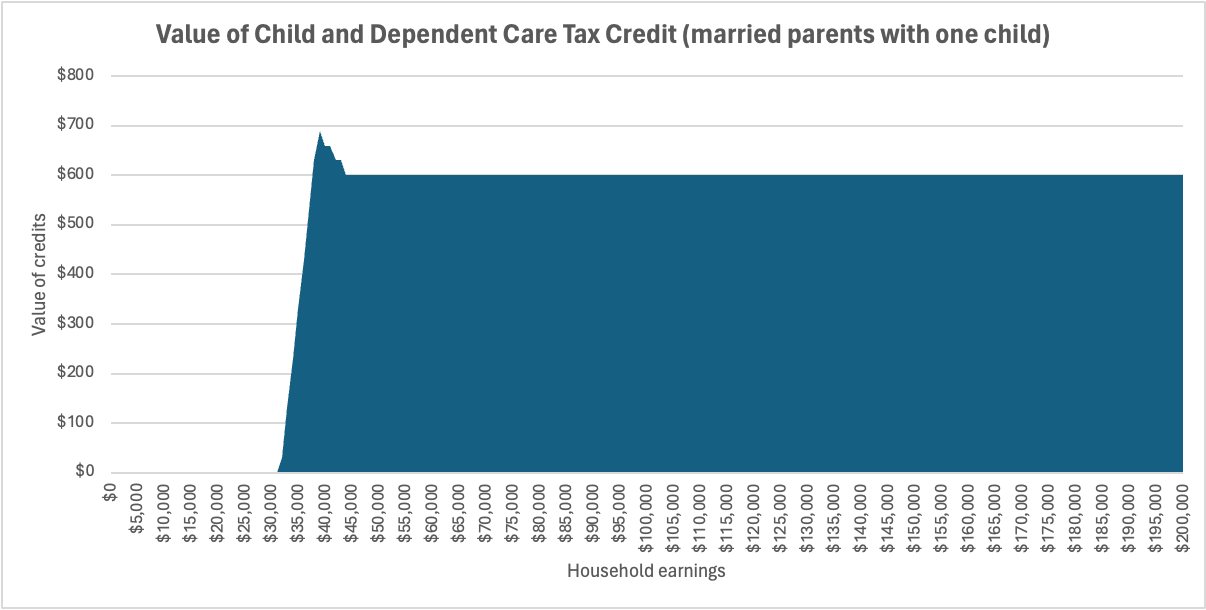

For married couples with two incomes, the CDCTC is even further out of reach (see Figure 6). The CDCTC is essentially off-limits to the parents, married or single, who are least prepared for the cost of child care and who have the most to gain from access to the workforce.

Figure 6

In order to claim the credit, parents must have documented expenses from an eligible care provider. Parents must submit their total expenses and the Employer Identification Number (EIN) or SSN of their care provider as part of their tax filings. Formal, center-based care is usually the most prepared to help parents with these filings. Parents relying on less formal paid care will need to track what they pay a sitter or their nanny on their own and also ask for their caregiver’s full Social Security Number. A plurality of parents report in surveys and in practice that they prefer to place their young children with a relative during the work day, rather than formal, center-based care.24 The CDCTC makes the most popular choice for care an uncompensated choice. It functions as an income transfer from parents seeking more informal care (often poorer families) to those who prefer more formal care (often richer ones).

The tax credit only reaches a narrow slice (one in ten) of tax-paying households with eligible children. Low-income working families are most likely to miss out on the credit. Nearly half (44 percent) of the money paid out in CDCTC claims goes to households making more than $100,000. Only about 3 percent goes to families making $25,000 or less.25

Finally, parents of larger families wind up systematically shortchanged. The CDCTC caps qualifying expenses at two children. A third child does not receive any credit for his or her child care expenses. There is no logic for treating siblings differently; parents managing care for three or more children deserve the same support for each child.

Furthermore, parents unable to claim the CDCTC end up doubly disadvantaged. They miss out on tax relief their peers may be eligible for, and they also face higher prices for child care. Evidence suggests when parents receive more in CDCTC funding, child care providers raise their prices accordingly. In one study of child care providers’ responses to expanded state CDCC funds (which parallel the federal CDCTC), for every additional dollar allocated to families, the cost of center-based care increased by at least $0.60. Eligible parents captured less than half the value of a CDCTC expansion. Ineligible parents ended up paying higher prices.26

Parents of young children would be better off with a simpler, more generous credit for young children – no matter what kind of care their parents choose. Parents could better anticipate how much support they’d receive and would be able to spend the money on the care that made sense for their family.

The most straightforward way to address each of these issues is to eliminate the CDCTC in conjunction with an expansion of the CTC.

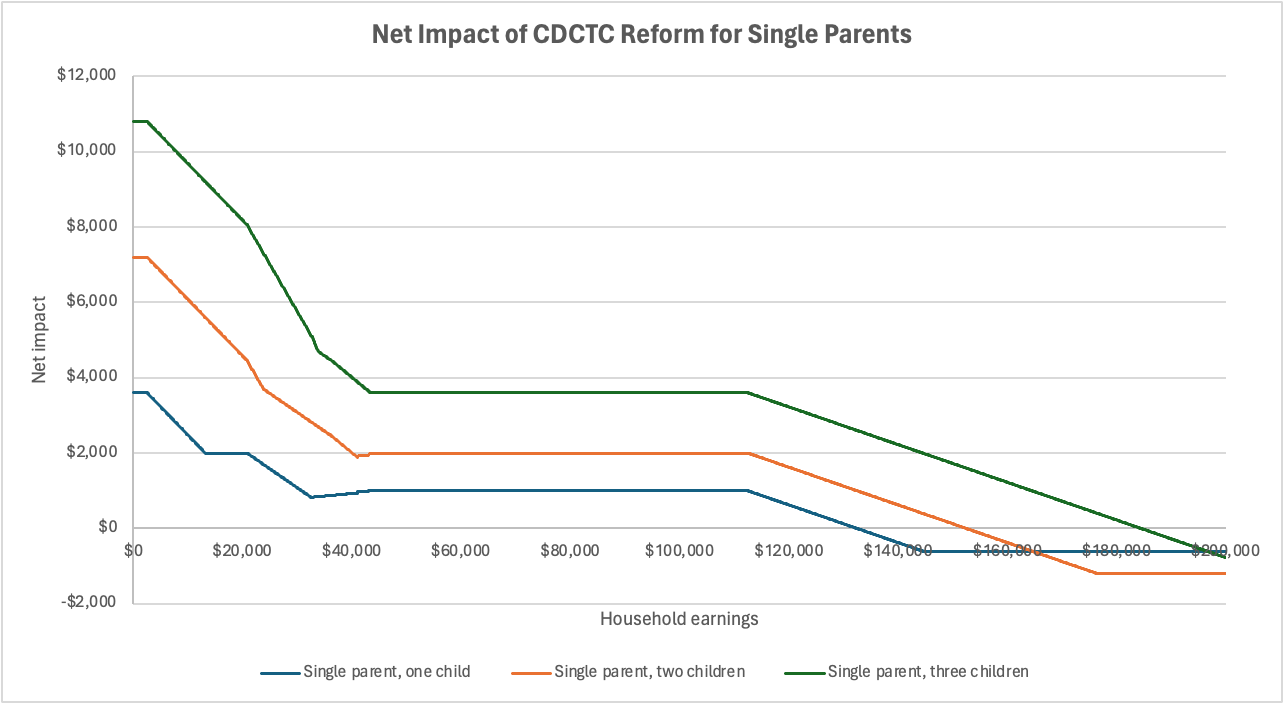

For low-income single parents, replacing the CDCTC with an expanded, fully refundable CTC would mean a substantial improvement (Figure 7). Most other single-parent households making below $130,000 would also be better off, with more money in their pocket, greater ease of claiming the credit, and more predictability regarding the amount they could claim. Upper-income families currently claiming the credit would see a net decrease, and it would be a modest adjustment, especially relative to their income.

Figure 7

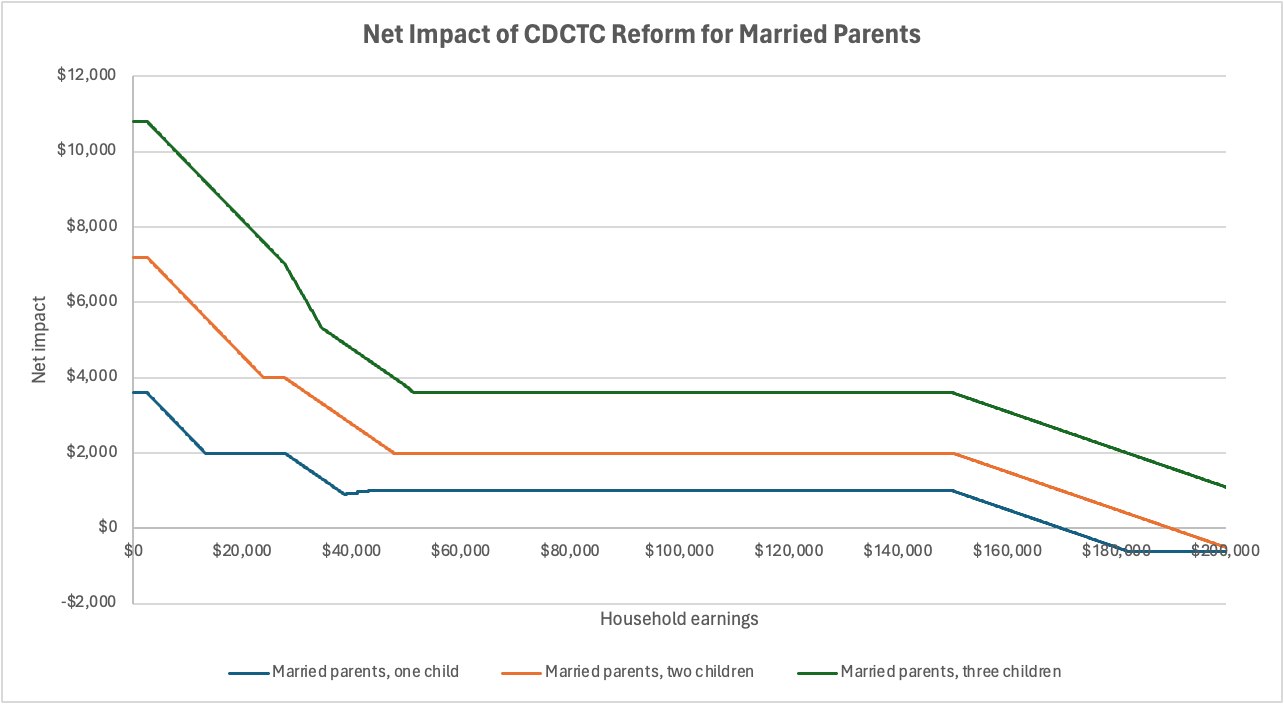

Similarly, all families with married caregivers would be better off receiving a fully refundable, expanded CTC versus a limited CTC and the current CDCTC. The only families who would see a decrease in their credits would be those with two or fewer children making more than $170,000 per year.

Figure 8

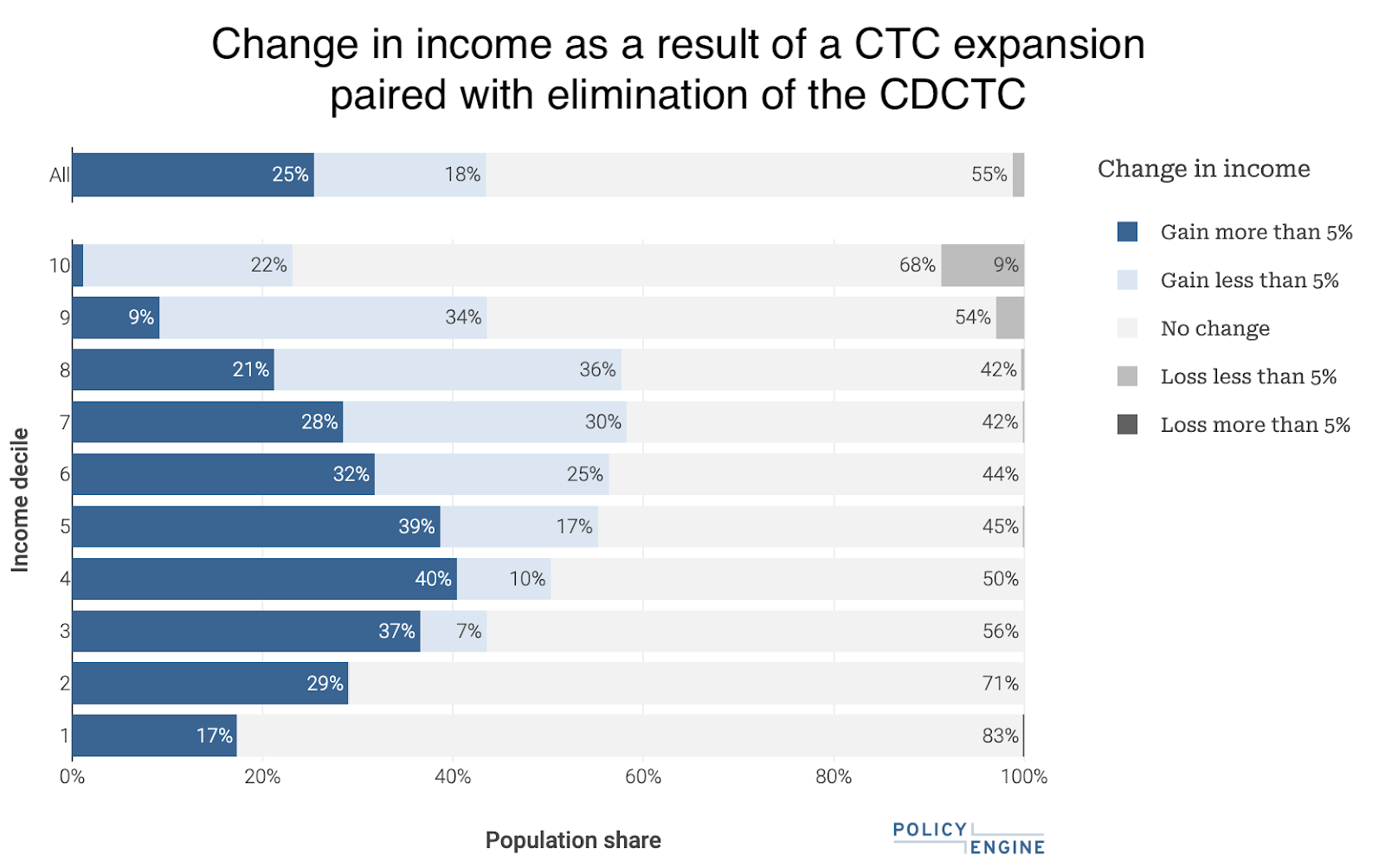

In our analysis, eliminating the CDCTC alongside an expansion of the CTC would cost an additional $105.9 billion in 2024—a savings of 4 billion—while it would still reduce child poverty by 31.2 percent — on par with our baseline.27 Figure 9 shows the distributional impact of the changes. 43 percent of the population would see a net gain in income, with the largest increases going to middle class households. Only 1 percent of households are made worse off in this scenario. They are in the upper deciles.

Figure 9

Supporting upward mobility by reforming the EITC

When the National Commission on Children published the landmark report mentioned in the introduction, many policymakers and academics were increasingly concerned that the structure of our tax and welfare programs was actively penalizing parents trying to do what was best for their children. No one should lose money, they argued, by moving from welfare to work and/or getting married to their partner.28 The crux of the problem was that parents who left welfare to take a full time job or who married a partner with a full-time job risked worsening their household finances either by losing some or all of their benefits or by paying higher taxes. These program structures created extremely high implicit marginal tax rates (IMTRs) that sometimes reached 100 percent—every dollar earned resulted in the loss of a dollar of benefits.

In the decade that followed, Congress made several major changes aimed at reducing work and marriage penalties for the lowest-income families. The most prominent were the 1996 welfare reforms, which reduced benefits, added new time limits and work requirements, and allowed states to shift block grant funds to work supports. Congress also undertook two major expansions of the Earned Income Tax Credit (EITC), in 1990 and 1993. Prior to that, families with children were eligible for a small credit that did not vary based on family size. The 1990 changes increased the size of the credit and varied it based on whether workers had one or two children. The 1993 changes again increased the size of the credit and expanded it to workers without children.29 These changes, in conjunction with a strong labor market, successfully reduced many of the work and marriage penalties that had hindered marriage or the movement from welfare to work.

But the changes had serious unintended consequences that created new work and marriage penalties for a different set of families. The EITC changes — along with the proliferation of state-level EITCs and the expansion of the Supplemental Nutrition Assistance Program (SNAP) — reduced (but did not eliminate) penalties for the lowest-income families by shifting them upward, onto working-class families.30 Congress provided partial relief from EITC marriage penalties in 2002, but they largely remain in place.

A wave of research in the years that followed these changes has chronicled how benefit phaseouts have penalized workers just above the poverty line by increasing IMTRs on work and marriage for families with children.31 Reforming the EITC is a good place to start for policymakers interested in reducing these penalties.

The EITC is a refundable tax credit for low-income workers. Depending on whether a worker has children and how many, the credit phases in at a steady rate as earnings initially rise, briefly plateaus at the maximum credit as earnings continue to rise, and then begins to phase out as earnings increase after a particular threshold until the credit amount reaches $0 again. Table 1 indicates the phase-in rate, maximum credit, threshold, and phaseout rate for families with one, two, and three or more children.

Table 1

| One child | Two children | Three + children | ||||

| Current | Reform | Current | Reform | Current | Reform | |

| Phase-in rate | 34% | 20% | 40% | 28% | 45% | 28% |

| Threshold for maximum credit | $11,750 | $13,500 | $16,510 | $14,000 | $16,510 | $14,000 |

| Maximum credit | $3,995 | $2,700 | $6,604 | $3,900 | $7,430 | $3,900 |

| Phaseout threshold | Single: $21,560Married: $28,120 | Single: $24,000Married: $48,000 | Single: $21,560Married: $28,120 | Single: $24,000Married: $48,000 | Single: $21,560Married: $28,120 | Single: $24,000Married: $48,000 |

| Phase-out rate | 15.98% | 12% | 21.06% | 15% | 21.06% | 15% |

Two features of the EITC are the primary sources of work and marriage penalties. First, after reaching the earnings threshold, each additional dollar earned results in the loss of about $0.16 to $0.21. This functions as an IMTR of 16-21 percent on families whose income puts them between 100 percent of 200 percent of the federal poverty line. The poverty trap of the 1990s has been replaced with a just-above-poverty trap.

Second, the threshold at which the credit begins phasing out for married parents ($28,120) is only $6,560 higher than that for single parents ($21,560). This creates a situation where single parents may lose thousands of dollars if they marry their partner. For example, an unmarried couple where each parent earns $20,000 stands to lose about $2,500 in EITC benefits annually if they get married.

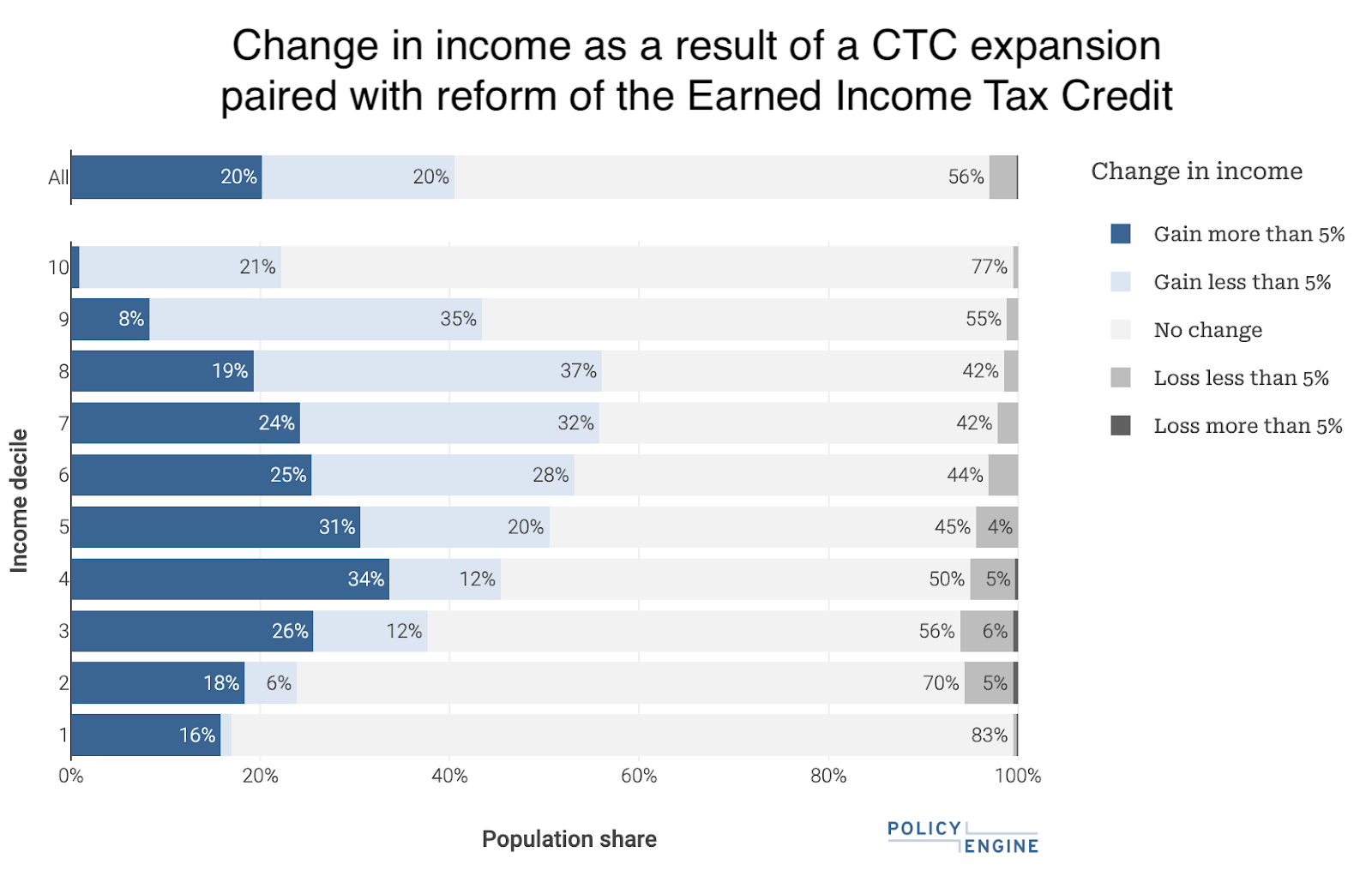

The most straightforward way to address each of these issues is to reduce the value of the EITC, increase the phaseout threshold, and reduce phaseout rates in conjunction with an expansion of the CTC. Table 1 offers one such set of reforms that would ensure families are kept whole or made better off.

First, the reform transfers much of the child portion of the EITC over to the CTC. The EITC add-on for each additional child shrinks considerably for the first two children and is eliminated altogether for the third. Moving toward separating the CTC and EITC into distinct credits aimed at low-income workers and children is in line with international practice and the recommendations of the Taxpayer Advocate and other tax experts.32

Second, the reform reduces phaseout rates from about 16 percent to 12 percent for workers with one child and from about 21 percent to 15 percent for workers with two or more children. This reduces work penalties for those at and above the poverty line. Lastly, the proposal reforms the phaseout threshold for married parents so that it is double that of single parents. That same unmarried couple, for example, where each parent earns $20,000 would not lose any EITC benefits annually if they get married.

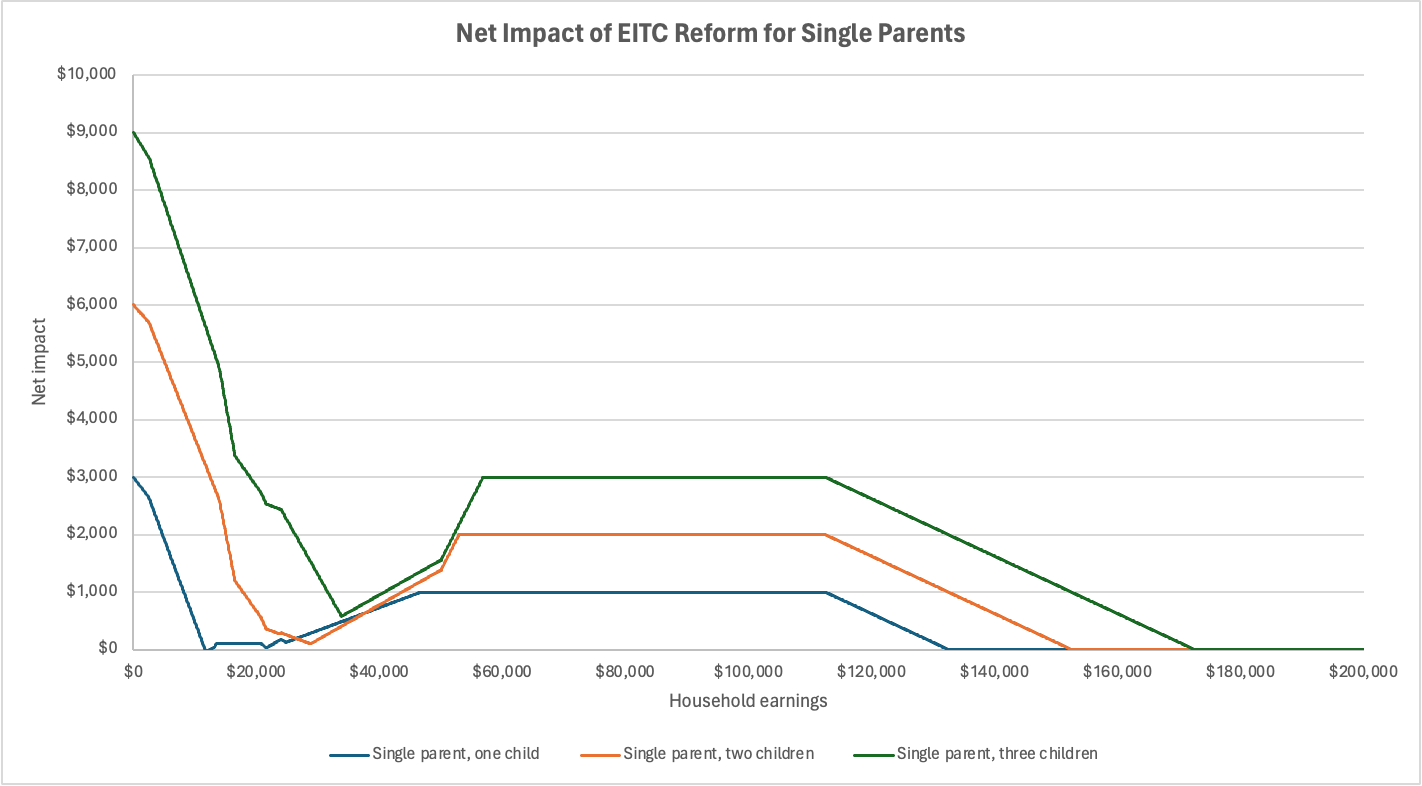

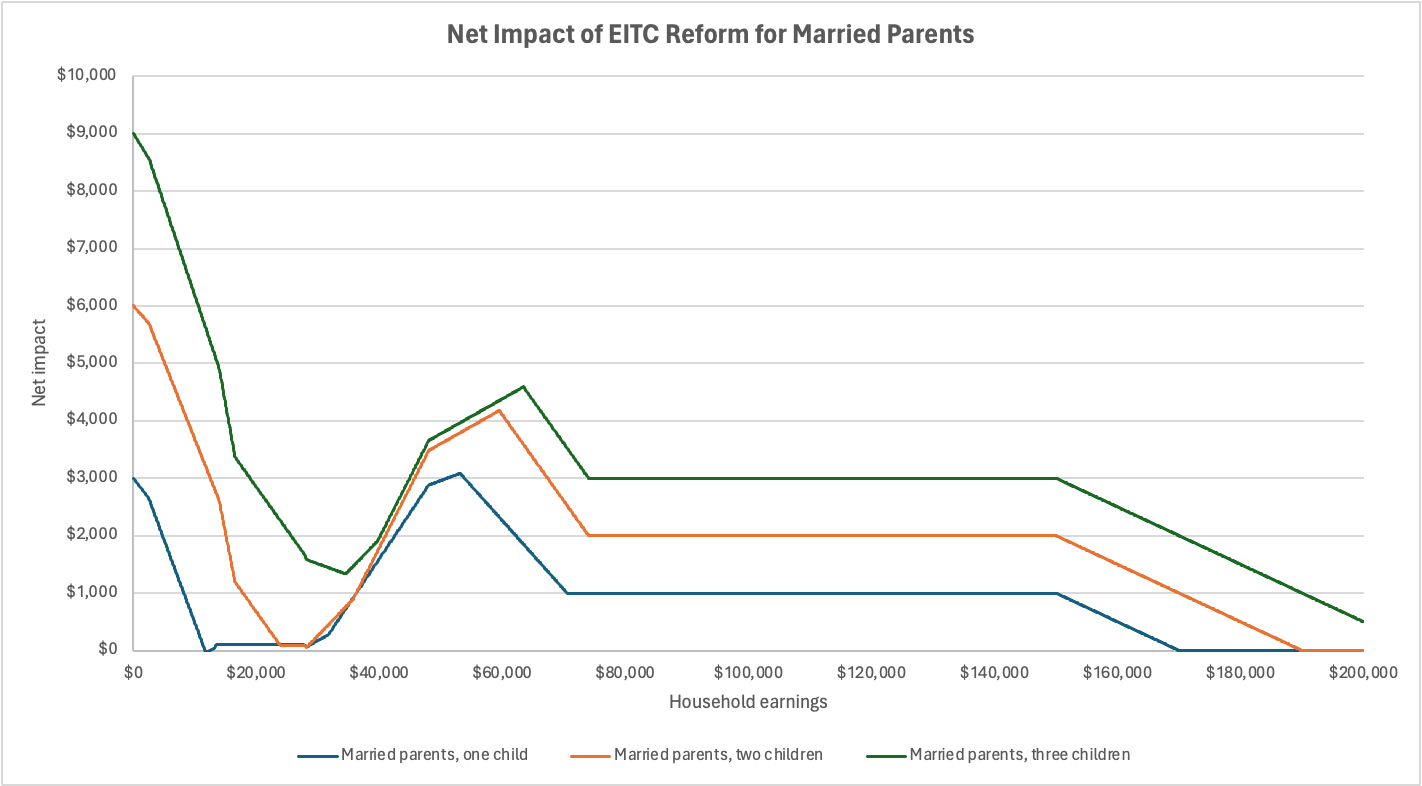

The distributional impact would depend on the value and structure of the expanded CTC. Figures 3 and 4 illustrate the net impact on single and married parents by income. It assumes children are older than six with each receiving a $3,000 credit. Under our proposed expansion, all families with children are held harmless33 or come out ahead in terms of total credit amounts. The poorest families and middle-class families see the biggest gains. Working-class families benefit from reduced work and marriage penalties.

Figure 10

Figure 11

In our analysis, shrinking the EITC alongside an expansion of the CTC would cost an additional $85.3 billion in 2024 — saving about $24 billion relative to our baseline. The combined reform would reduce child poverty by 23.4 percent, 7 percentage points lower than our baseline.34 Figure 12 shows the distributional impact of the changes. Forty percent of the population would see a net gain in income, with the largest increases going to middle-class households. Three percent of households are made worse off in this scenario, with most of them concentrated in the second through fifth deciles.

Figure 12

Conclusion

For families, the American tax code has become a maze of overlapping benefits that often work at cross-purposes. The goods these successive reforms sought to promote can be better achieved with a simpler structure that uses the CTC as the primary way to offer child-related tax benefits. Our analysis provides a menu of options for reducing poverty, work penalties, and marriage penalties while reducing tax code complexity through consolidation. Table 2 summarizes our cost and distributional impact findings for each of the options we considered.

Table 2

| Policy reform | Cost impact | Child poverty reduction | Net impact (gain/loss) |

| Baseline CTC | $109.7 billion | 31% | 44%/0% |

| CTC + HoH | $83.8 billion | 31% | 39%/4% |

| CTC + CDCTC | $105.9 billion | 31% | 43%/1% |

| CTC +EITC | $85.3 billion | 23% | 40%/3% |

Congress made some progress by consolidating two of the five major family tax benefits in 2017, but those changes are temporary and set to expire at the end of 2025. Our findings suggest there is still much to be gained by considering further rounds of family tax benefit consolidation. Each of the options we consider here keep the poverty impact of a more generous CTC while reducing overall costs, complexity, and work/marriage penalties.

About the authors

Joshua McCabe is the Director of Social Policy. He focuses on issues related to child poverty and household stability. McCabe previously worked as an Assistant Professor of Sociology and Assistant Dean for Social Sciences at Endicott College. McCabe’s work has been featured in the Washington Post, the National Review, the Hill, and more. McCabe has received his B.A. in Political Science from Emmanuel College, his M.A. in Regional Economic and Social Development from the University of Massachusetts, Lowell, and his Ph.D. in Sociology from the State University of New York at Albany.

Leah Sargeant is a Senior Policy Analyst who works on family economic security with the social policy team. Previously, Sargeant worked to facilitate debates on college campuses for Braver Angels and as a reporter for Five Thirty Eight. Her writing has appeared in the New York Times, the Washington Post, National Review, and more. Sargeant received her B.A. in Political Science from Yale University. She is the author of two books.

This post was originally published on 3rd party site mentioned in the title of this page